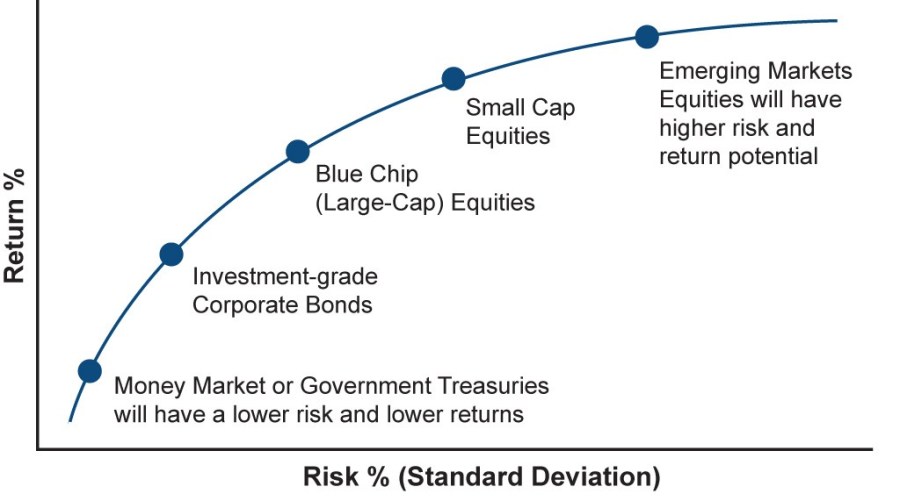

Some of you have read Get Rich Slowly and though: no, this is not slow enough. The dizzying pace of 6-7% annual return is too much. You want more safety and less volatility, something towards the bottom-left corner of the efficient frontier.

Concrete example: you have $10,000 today, and you may want to spend them sometime in the next 2-3 years on a car, a mini-retirement, or just an emergency. You would like there to be more than $10,000 when you need the money, but what you really want is to be confident that there wouldn’t be any less than that. Emerging market stock index funds can turn $10,000 to $15,000 in two years, or to $6,000. You just want there to be $10,500.

This post will briefly cover the basics of low-risk-low-return saving, with general principles and particular examples. With apologies to my international readers, the examples are all USA-specific. The general approach, however, should be easily transferrable – and you’ll know what scams to watch out for.

“Risk-free” rate

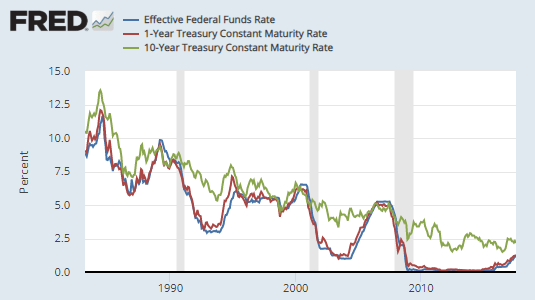

The benchmark for the return rate on low-risk investments is the federal funds rate, which is currently set by the Federal Reserve at 2.5%1. This is the rate at which big institutional banks borrow dollars2 from each other and from the central bank overnight. This number also tracks very closely the rate at which the US government borrows money for one year.

The chance of any bank going bankrupt overnight or the US government defaulting on its debt within 1 year are both very close to zero, which is why the federal funds rate is often referred to as the “risk-free rate of return”. Of course, nothing is ever truly risk-free when finance is concerned. “Risk-free” is a euphemism for “this won’t blow up unless the entire rest of the financial system blows up as well, and at that point you should care about your stocks canned food more than about your dollar savings.”

So, big banks can borrow and lend “safely” at 2.5%. Let’s see what normal schlubs like us can get when we go to the big banks ourselves.

Checking and Savings Accounts

There are roughly 70,000 retail bank branches in the United States. A third of them belong to the biggest 5 retail banks: Wells Fargo, JP Morgan Chase, Bank of America, US Bank, and PNC. Either one would be happy to open you a checking account – a simple account where your money is insured by the government, accessible from any ATM and online, and earns 0% interest.

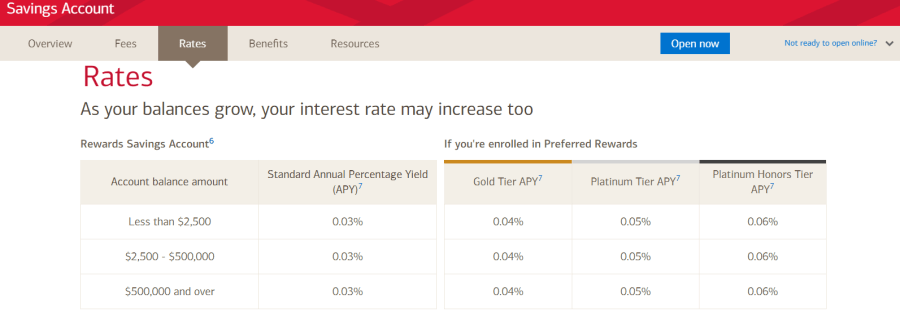

When the bank sees that your pockets are bulging with 100 Benjamins, they will offer to open you a savings account as well. Savings accounts usually have limitations such as a minimum balance needed to open, a cap on monthly transfers, and fees. On the plus side, your money will earn an astonishing interest rate of… 0.03%.

That’s right, at the end of two years in a Bank of America savings account your $10,000 will accrue six whole dollars! If you reach the Platinum Honors Tier, which requires an endless amount of bureaucratic hoops to jump through and also sacrificing your firstborn to Mammon the prince of Hell, they will toss in an extra $6 and a lollipop.

And then, they’ll charge you $192 in monthly service fees.

Actual rate of return: negative 2%.

Scam meter: totally a scam.

Certificates of Deposit at Big Banks

0.03% interest will double your money in a mere 2,310 years, not counting taxes. If that’s a bit too slow, banks will offer you a certificate of deposit, or CD. CDs offer a higher rate of return in exchange for placing more limits on your money. CDs have a set maturity date and withdrawing money prior to that date incurs a penalty. In the few places I’ve checked, the penalty is about a quarter of the total interest that would be earned for the full term.

CD rates at the big banks vary from 0.1% at Bank of America to 2% at Wells Fargo if you lock the money down for two years. So $10k in a Wells Fargo CD will turn into $10,201 after two years, or $10,050 if the money is withdrawn after one year: $100 of interest minus $50 in early withdrawal penalty.

There may also be fees associated, and interest on CDs is taxed as income. Marginal income tax rates are between 22%-37% for Americans earning $38,000 or more, so even in the best case scenario a two year CD will only net $201 * (1-.22) = $157.

Actual rate of return: 0-1.5%.

Scam meter: only a bit of a scam.

Savings Accounts and CDs at New Banks

Nerdwallet has a list of rates offered on CDs and savings accounts at various institutions. The bigger established banks are clustered towards the end of the list, while the top of it is populated by smaller, newer, and online-only banks looking to aggressively grow their customer base. Some of these banks offer 2% on savings accounts and 2.6-2.7% on CDs. If you think there’s a chance you may need the money before the CD matures, the two options are probably equivalent in terms of expectancy.

In any case, if you want a high-yield account with a bank it makes sense to shop around for a young bank desperate for love, not one of the old fat cats.

Actual rate of return: 1.5-2% after tax.

Scam meter: barely a scam at all.

CD Secured Loans

If you do open a CD, and especially if you ask about withdrawing the money early, the bank will start marketing to you a miraculous financial product called a CD secured loan. Are you cynical enough to guess what that is?

The bank, via a well-dressed “relationship technician” or a brochure with glossy print, will inform you that while normal bank loans have an interest rate of 10-12%, you can get a loan at interest rates of just 4-8% as long as it’s fully secured by your CD. In case it’s not clear: the bank will give your own money back to you, with zero risk to the bank itself (since the loan is fully collateralized), while charging you 2-6% interest for the pleasure.

And if you ask why on Earth you would pay 6% interest on your own money when you can just withdraw it and pay 0% at worst, the bank will tell you about the wonders it will do for your credit score3. At this point I recommend shouting “Begone, demon!” at the top of your lungs and running out of the bank branch while your soul is still intact.

Actual rate of return: negative 6%.

Scam meter: Shameless and disgusting scam. I wrote 5,500 words defending the finance industry but then added a caveat: finance turns bad when it collides with the astounding financial illiteracy of the average American. CD secured loans are as bad an example of this as I know. It’s a financial product designed solely for people who are easily persuadable, financially ignorant, and flunked middle school math.

Index Funds

By and large, the best tool for low-yield investments is the same as the best tool for high-yield investments: index funds. Instead of lending money to a single bank, bond ETFs (exchange traded funds, the easiest way to invest in indices) allow you to buy pieces of loans to the US government and other low-risk institutions.

Because of their equity-like structure, the value of ETFs is a bit more volatile day-to-day but on a scale of a year or more bond ETFs basically replicate the yield of the underlying bonds. If an ETF just keeps buying treasuries that have 2% yield, the ETF will inevitably yield 2%. More importantly, ETF gains are taxed at the capital gains tax rate (15% if held for more than one year) instead of as income tax (22%-37%).

Two great options are Vanguard’s money market fund, VMFXX, and bond fund, VBMFX. VMFXX holds short-term US government treasuries and bank repos, with an expected yield of around 2-2.5%. VBMFX holds two-thirds long-term US treasuries and one-third corporate bonds. The expected return is around 3% today, but the average maturity of the bonds is 8 years which can lead to some short-term divergence between the ETF return and the bond yield if interest rates change.

Actual rate of return: 2-2.5% after taxes and Vanguard’s tiny fees (0-0.15%).

Scam meter: Basically, everything Vanguard does is the opposite of a scam. RIP Jack Bogle, the trillion-dollar real-life Robin Hood.

Wealthfront

Investing is a story of trade-offs. High-returns, low volatility, low tail-risk, flexible access to money – you have to pick some and compromise on the others. You can’t have a return higher than the federal funds rate, zero volatility, FDIC insurance, and no-limit access to your cash at any time.

Oh, wait, you totally can with Wealthfront.

The Wealthfront cash account offers 2.51% return with no fees, FDIC insurance up to $1,000,000, and unlimited free transfers. I swear they’re not paying me to recommend them (although I do get a small bonus if you use my referral link). I just researched financial brochures for several hours, and then Wealthfront just turned out to be better than every single bank on practically all parameters.

I’m not entirely sure why this is the case. It could be that Wealthfront just has much lower costs, being a small startup with no physical branches or fancy investment managers with MBAs. Perhaps they’re eating through some VC money in the hunt for market share growth. And perhaps, the number of Americans who can actually do the math and figure out the best deal is so small that every big bank would rather spend money on marketing to idiots than on paying their customers actual interest on deposits.

My goal to expand the number of the financially literate, one blog post at a time.

Footnotes

[1] All rates in this post are in annualized terms, so 2.5% means 2.5%-a-year.

[2] Other currencies have different rates set by their respective central banks.

[3] The credit score system is itself a meta-scam. It’s a way for financial institutions to sucker you into paying interest on debt, which is good for them and bad for you. You can build up an OK credit score by doing sensible things like opening a few good credit cards and paying them off every month with no interest. But then, once you’re emotionally invested in the system, the only way to improve your score is to take on debt with interest.

Spoiler alert: the way to pay less interest is to pay less interest, not to pay more interest in order to “build up your credit score”.

Great post.

Re: index funds, VBMFX is closed to new investors, but that’s because Vanguard replaced it with VBTLX, which is identical aside from having a lower expense ratio.

One thing to be aware of with VMFXX is that it pays out all of its gains as ordinary dividends, so it isn’t taxed at the capital gains rate. VBTLX is a mixture of capital gains and ordinary dividends.

LikeLiked by 1 person

You can buy treasury bonds directly from treasurydirect.gov

LikeLike

Have you considered updating your previous Get Rich Slowly post? When I try to open a Wealthfront account I get lots of options that sound reasonable (i.e. let Wealthfront play with your actions to try and minimize the taxes you pay) but stray more and more from a passive index strategy. My limited financial knowledge led me to freeze in confusion, which sounds suboptimal.

LikeLike

The tax stuff is all good, just say yes. As for things like “risk parity” and “smart beta”, I don’t know how much they help but I doubt they can really hurt. There’s no real “pure index” that one should follow, any indexing/reinvesting/tracking strategy involves making some choices (why S&P 500 and not S&P 613?)

In any case, the difference between WF with and without these options turned on is probably ~1% of the difference between WF and paying 2% fees or holding cash.

LikeLike

In the time since this post was written, the “risk-free” federal funds rate has lowered from 2.5% to 0.25% (as of 2020-11-23). So investments don’t need as high a rate of return to beat the federal funds rate, but presumably most bank accounts will offer worse returns, since banks now make less money from inter-bank lending.

Another thing that has changed: Wealthfront’s cash account no longer offers that high 2.51% annual return. Its current interest rate is 0.35% APY. I can see that the rate was indeed 2.51% around the time of this post, then gradually dropped to 0.26% over ten months before rising to 0.35%, which it has stayed at for six months. The federal funds rate was lowered from 1.75% to 0.25% around the same time as the Wealthfront cash account’s drop to 0.26% APY.

Putting these facts together, Wealthfront’s cash account with 0.35% returns still beats the federal funds rate of 0.25%, and it hasn’t lost the benefits of no fees, FDIC insurance up to $1,000,000, and unlimited free transfers. But there might now be other safe investments that do better. The rate of 0.35% APY puts Wealthfront’s cash account at rank 16 out of 59 on your linked NerdWallet list of bank accounts sorted by APY with the default filters. Those 59 bank accounts have interest APYs ranging from 0% to 1.25%.

LikeLiked by 1 person

I actually signed up for Wealthfront from this post… kind of. I noticed an arbitration opt-out clause in their TOC, which I read all like 200 pages of, and emailed them to initiate it. They told me they were not offering “custom contracts” at this time and that the arbitration opt-out would not be honored. When I replied that the contract said that communications by email or other channels would not be deemed valid, they said that I could either close my account or they would forcibly.

I really wanted to use their service, since it seemed like something interesting that was a good idea and would be beneficial. I guess I am looking at other options though, because I will not store my money with a company that treats their own contract like a cage for me but a weapon for them.

If anyone has further information on this, I turned on replies for comments.

LikeLike

It’s worth considering inflation. If the rate of inflation is higher than the risk-free rate (as it is right now), then investing in T-bills or high-yield savings accounts is more like “get poor real slowly”. At one point in the 20th century, T-bills experienced a 50% drawdown in real terms.

Is there a “get rich real slowly” portfolio that works even after adjusting for inflation? I don’t think so, at least I don’t think there’s any portfolio that gets a guaranteed positive real return. If I was super risk-averse, I’d invest in something like Harry Browne’s Permanent Portfolio: 25% T-bills (or high-yield savings account), 25% bonds, 25% stocks, 25% gold. The stocks and gold might save you during inflationary periods, and the T-bills will save you during a market crash. As a hedge against total financial collapse, I might hold the gold physically (but then there’s a risk of burglary, I’d guess is more significant than the risk of financial collapse).

LikeLike

Jacob, could you please share the structure of your investment portfolio, and how it performed compared to Permanent Portfolio/SP500?

LikeLike